- Customer Service

TD First Class SM Visa ® Signature Credit Card

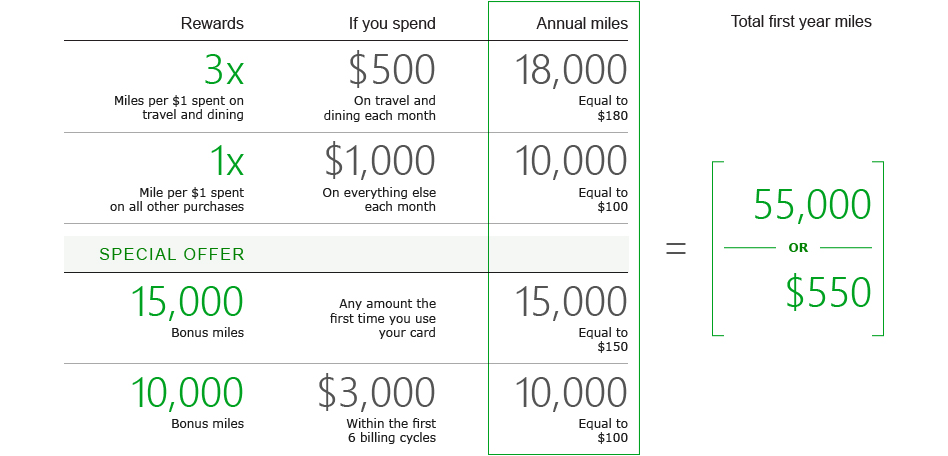

Travel rewards – Earn triple miles on travel and dining

Compare TD cards >

Read complete terms and conditions for details about APRs, fees, eligible purchases, balance transfers and program details.

Offer details, rates, fees and terms

Bonus miles offer.

Earn up to 25,000 bonus miles within the first 6 billing cycles of account opening, which equals a $250 statement credit towards travel or dining purchases

Bonus miles will be reflected on your credit card statement 6 to 8 weeks after a qualified first purchase and/or 6 to 8 weeks after $3,000 in total net purchases made within the first 6 billing cycles of your credit card account opening date. This offer is non-transferable. This online offer is not available if you open an account in response to a different offer that you may receive from us. This online offer is not available if you open an account in response to a different offer that you may receive from us.

Rewards details

3X First Class miles on travel and dining purchases , including flights, hotels, car rentals, cruises and dining, from fast food to fine dining

1X First Class miles on all other purchases – no categories or gimmicks and earn points that never expire as long as your account is open and in good standing.

Rates and fees

Need more information?

Take a look at our terms and conditions or personal cardmember agreement .

Earn unlimited points with every purchase, and triple the miles on travel

See how many miles you can earn from travel and other purchases.

Redeem your First Class miles for a statement credit toward travel and dining purchases >

To earn and redeem points, your account must be open and in good standing.

Credit Card FAQs

Manage your card, security you can count on.

Don't worry-we're protecting your every move. Our built-in chip technology helps guard you against fraud. Plus, you get the benefits of Visa Zero Liability 2

Managing your account is easy

Get the service you need, when you need it. Log in to your account or talk to a TD Bank representative 24/7 at 1-877-468-3178.

Redeem your rewards

Visit the td first class rewards site >.

- Small Business

- Private Client Advice

- British Columbia

- New Brunswick

- Newfoundland Labrador

- Northwest Territories

- Nova Scotia

- Prince Edward Island

- Saskatchewan

- English Selected

- secure Login

Get a quote

Home/ Condo/ Tenant

Why Could Travel Insurance Be Important for Canadian Seniors and Snowbirds?

While Canadians have always enjoyed travelling, both domestically and internationally, after the last couple of years, the pace and volume of travel has increased. Among these travellers is a certain group that partakes in travelling more than the rest, especially during the winter—the senior travellers, aka "snowbirds".

Who are considered senior travellers, you ask?

While travel doesn't exactly have an age limit, people who've joined the I'm-in-my-60s and above club could be considered seniors in Canada. As the name might suggest, "snowbirds" usually try to escape the winter by heading off to a warmer destination by flight or even by road in RVs. Favourites include the more southern areas of the USA, like Arizona, Florida, Texas, and California. Some adventurous souls even take off for exotic places like Mexico, Costa Rica, Ecuador, Portugal, and the Caribbean.

This lifestyle is quite exciting, but there are several things to consider before you plan such trips. One of the many things on that list includes travel insurance, which leads us to our next question:

Do seniors need travel insurance?

While happiness may likely be at the top of one's agenda during these trips, preparedness should also share the spot. Young or old, everyone has different needs for their trips, and leaving your country or even your province of residence may leave you open to medical costs due to accidents or mishaps. A travel insurance plan could be of help.

Why can travel insurance be important for seniors?

As seniors may be more susceptible to injuries or physical harm than younger people, there are several things to keep in mind when travelling outside of your province of residence or Canada when it comes to health insurance. Your provincial health insurance may not be available to cover all your medical costs abroad or out of your province. In which case, you will have to pay the bills. If certain criteria are met, you might get some of the expenses reimbursed.

Also, if you are depending on your credit card to take care of medical bills, it's important to understand that the travel medical insurance that comes with your credit card may have a lower coverage period for older cardholders. You should review the details of the travel medical insurance that comes with your card and, if needed, purchase additional travel medical insurance to cover the entire length of your trip before leaving.

When is the right time to get travel insurance?

You can apply for travel insurance before you depart on your trip.

Tips for getting travel insurance as a senior

Like everything else in life, it's always good to know what you're paying for. Here are a few things to look for when getting travel insurance as a Canadian senior or snowbird:

- Consider what kinds of emergency travel medical expenses are included. For example, hospital fees, ambulance services, prescription drugs, medical appliances, etc.

- What kind of non-medical coverage are you getting? Will you have coverage for trip cancellations or interruptions, lost luggage, and delays?

- Are emergency dental costs covered?

- What's the duration of your coverage?

Some factors in calculating the cost of travel insurance

The cost of travel insurance can depend on many factors, which vary by insurer. A few of these factors may include your age, sex, and health condition. You can always check your policy or speak with a licensed travel insurance advisor to get details. At TD Insurance, some of the factors we consider include:

- Health and age : as we grow older, we may be more likely to have health risks when compared to our younger selves. For that reason, travel insurance for seniors can be more expensive because, as the age increases, so does the level of risk, leading to comparatively higher rates.

- The type of coverage : there are several types of travel insurance plans, like single trip, multi-trip, and travel plans that include both medical and non-medical coverage. Since the coverages vary, the premium will vary too.

- Number of people covered under the travel policy : for instance, a family plan might cost more than a plan just for an individual as more people will be insured under a family plan. However, a family plan could be less expensive than purchasing separate plans for each member of your family.

- The duration of the coverage : the longer your trip is, the more it will cost you to get insured.

Ways to save - are you a frequent traveller?

If you find yourself in the frequent traveller category and have planned multiple trips for the year, you could benefit from a plan more suited to that nature, like the TD Insurance multi-trip all-inclusive plan or the multi-trip medical plan . They may be more cost-effective than purchasing an individual plan for each trip.

TD travel insurance and seniors/ snowbirds

The adage "age is just a number" might be true when it comes to planning adventures, but with that number come certain important changes in our lives and travel insurance as well. When it comes to the age limit, here are a few things to remember:

- With a plan like the TD Insurance Multi-Trip All-Inclusive Plan 1 , if you are 60 years of age or older, you may choose the length of each trip to be 22 or 30 consecutive days. Take a look at the sample policy for a better understanding.

- If you are over 80, the TD Insurance Multi-Trip Medical Plan 2 gives you the option to choose between 4, 9, or 16 consecutive days for each trip. Here's a sample policy for a closer look.

As a senior traveller, consider a travel insurance plan best suited for you. You can start making plans and take a look at the travel insurance policies offered by TD Insurance .

We would also encourage you to stay updated with the travel advisories to be aware of changing circumstances that may alter your travel plans.

Related articles

TD Insurance Trip Cancellation & Interruption Plan

Coverage & exclusions: what you may want to consider

Understanding Travel Insurance Terminology

Share this article

The content on this page is for general information purposes only and does not constitute legal, financial, or insurance advice. Speak to a licensed professional advisor regarding your specific situation.

The information contained herein, is subject to change without notice.

1 TD Insurance Multi-Trip All-Inclusive Plan is an individual plan underwritten by TD Life Insurance Company (medical covered causes) and TD Home and Auto Insurance Company (non-medical covered causes). Coverages and benefits are subject to eligibility conditions, limitations, and exclusions, including pre-existing medical condition exclusions. Please refer to the Sample Policy for full details.

2 TD Insurance Multi-Trip Medical Plan is an individual plan underwritten by TD Life Insurance Company. Coverages and benefits are subject to eligibility conditions, limitations, and exclusions, including pre-existing medical condition exclusions. Please refer to the Sample Policy for full details.

See you in a bit

You are now leaving our website and entering a third-party website over which we have no control.

TD Bank Group is not responsible for the content of the third-party sites hyperlinked from this page, nor do they guarantee or endorse the information, recommendations, products or services offered on third party sites.

Third-party sites may have different Privacy and Security policies than TD Bank Group. You should review the Privacy and Security policies of any third-party website before you provide personal or confidential information.

Sorry, we do not offer this product in the selected province

Please visit our homepage to see products available in your province.

- Personal Finance

The TD First Class Travel Visa Infinite Card and its travel insurance benefits

Insurance Coverage

First, it is very important to read the most recent version of the TD First Class Travel Visa Infinite Card Benefits Coverage Guide .

They can change at any time and it is your responsibility to be aware of these insurance benefits .

If you have any questions, please contact TD Customer Service at 1-866-374-1129 . It is strongly recommended that you call them before booking travel with your card and before you leave on your trip.

Eligibility

Travel insurance coverage is only available to :

- Primary cardholder

- Spouse and dependent children of the primary cardholder

- Additional cardholder

- Spouse and dependent children of the additional holder

In addition, the card account must be in good standing . This means:

- The Primary Cardholder has not asked TD to close the Account

- TD has not suspended and revoked credit privileges or closed the account

Eligibility Tool

To make it easier to understand the insurance coverage of its credit cards, TD has put together an interactive tool on travel insurance . In 6 questions, you can quickly find out if you qualify or not, when you pay in full for the trip in cash.

TD First Class Travel Visa Infinite Card Description

Travel medical insurance.

The maximum benefit for emergency medical care is $2,000,000. To be eligible, you only need to have the card, as per the Eligibility section above. This includes the following inclusions:

- Hospitalization

- Physician’s fees

- Private nursing

- Diagnostic services

- Ambulance and air ambulance services

- Prescription drugs

- Accidental dental and emergency relief of dental pain

- Medical Appliances

- Emergency return home

- Transportation to the bedside and compensation for the bedside companion

- Compensation for the travel companion

- Meals and accommodation

- Incidental hospital expenses

- Vehicle return

- Repatriation of deceased

- Baggage return

Trip cancellation and trip interruption insurance

To receive the benefits of this insurance coverage, the full cost of your trip must be paid with your ® Visa Infinite* Card" href="https://milesopedia.com/en/go/td-first-class-travel-visa-infinite-card-qc/" rel="noindex">TD First Class Travel ® Visa Infinite* Card and/or TD Rewards points.

A trip cancellation occurs before departure .

A trip interruption occurs on or after the departure date when the trip has begun .

Eligible reasons may be:

- The death of an insured person or an immediate family member

- A sudden, unexpected illness or accidental injury to a person or a member of his or her immediate family

- A natural disaster at the insured person’s principal residence

- Weather conditions during the trip

Common Carrier Travel Accident Insurance

To be eligible for this insurance, you must:

- Privileges under your account have not ceased or been suspended

- The account is not more than 90 days past due

- And the TD credit card must be in good standing

A common carrier is a land, air or water conveyance that is authorized to carry passengers for compensation. This can be a :

- Ferry or Cruise ship

- Bus or Train

- Cab or Limousine

If there is an accidental death or dismemberment, the maximum benefit is $500,000 .

Delayed and Lost Baggage Insurance

In order to benefit from this insurance, the credit card must have been used to pay 100% of the airfare .

Flight and travel delay insurance

To benefit from this insurance, at least 75% of the cost of your trip must be charged to the ® Visa Infinite* Card" href="https://milesopedia.com/en/go/td-first-class-travel-visa-infinite-card-qc/" rel="noindex">TD First Class Travel ® Visa Infinite* Card .

The reason for the delay may be due to weather, an outage or a strike for example.

This flight or travel delay insurance can be up to $500 , for a delay of 4 hours or more .

Hotel/Motel Burglary Insurance

This is for hotel and motel reservations in Canada and the United States only. At least 75% of the total cost of the stay must be charged to the card. The use of TD Rewards points is also valid under certain conditions.

The maximum amount is $2,500 .

Collision and damage insurance for rental vehicles

- Pay for the car rental at the rental agency with the ® Visa Infinite* Card" href="https://milesopedia.com/en/go/td-first-class-travel-visa-infinite-card-qc/" rel="noindex">TD First Class Travel ® Visa Infinite* Card MD (payment with TD Rewards points is accepted, under certain conditions).

- Refuse to purchase the Collision Damage Waiver (CDW ) or an equivalent coverage from the rental agency and have it written into the contract

The car rental covers up to 48 consecutive days and the manufacturer’s suggested retail price (MSRP) of the car must be under $65,000 . Some types of vehicles are not insured.

Purchase Assurance and Extended Warranty Protection

Purchase insurance covers items purchased with the ® Visa Infinite* Card" href="https://milesopedia.com/en/credit-cards/td-first-class-travel-visa-infinite-card-qc/" rel="noindex">TD First Class Travel ® Visa Infinite* Card for 90 days from the date of purchase . If the item is lost, stolen or damaged, it will be replaced or repaired with this insurance.

Extended warranty protection extends the manufacturer’s warranty up to one year . It begins after the manufacturer’s warranty expires and the item must be purchased with the Card.

Mobile Device Insurance

Did your new smartphone or tablet have a major accident and stop working? Mobile device insurance can come to the rescue, up to a maximum of $1,000 in reimbursement!

To qualify, at least 75% of the total cost of the device must be charged to the TD First Class Travel Visa Infinite Card. Under certain conditions, insurance is also eligible if the total cost of the device is financed through a plan with monthly payments .

Emergency travel assistance services

It is not really an insurance, but rather a help to solve a problem during a trip in unknown land. They do not offer payment or refunds. They are more of a medical second opinion or will tell you what to do if you don’t know what to do when you are in total panic.

The phone number is 1-800-871-8334 for Canada or the United States. Or if you are in another country: 1-416-977-8297 (collect).

This phone line can be useful for the following situations:

- Medical consultation and follow-up

- Medical emergency travel and medical referrals

- Payment to medical service providers

- Assistance in case of lost luggage

- Legal assistance

- Replacement of lost tickets and documents

- Translation Services

- Emergency transfer of funds

What to do if you have an insurance claim with the TD First Class Travel Visa Infinite Card

You must call 1-866-374-1129 , within the time frame following the date the event occurred.

In summary, here are the various insurance coverages of the ® Visa Infinite* Card" href="https://milesopedia.com/en/go/td-first-class-travel-visa-infinite-card-qc/" rel="noindex">TD First Class Travel ® Visa Infinite* Card :

Bottom Line

In addition to all this insurance to prevent inconvenience, the ® Visa Infinite* Card" href="https://milesopedia.com/en/go/td-first-class-travel-visa-infinite-card-qc/" rel="noindex">TD First Class Travel ® Visa Infinite* Card has a very profitable welcome offer from TD Bank .

With all these points, you can afford to get a stay that will not cost much. This is in addition to his annual TD Travel Credit of $100 for Expedia for TD bookings of $500 or more.

To save on travel and insurance, this is a secret card to have in your wallet!

All posts by Caroline Tremblay

Suggested Reading

4 times your credit card's travel insurance can help with summer travel woes, and 7 times it won't

Update: Some offers mentioned below are no longer available. View the current offers here .

Travel is more unpredictable than ever this summer. I've been lucky that none of my summer trips so far have been incredibly affected by delays or cancellations. But, air travel is a total nightmare right now , and staffing is still an issue for many travel providers — so it's likely only a matter of time.

Other TPG staffers have recently experienced issues. For example, TPG's Sean Cudahy got caught in last week's travel mess , while TPG's Nick Ewen spent time in New Jersey instead of Greece due to weather-related delays.

If you've been reading TPG for a while, you may already know that some credit cards provide travel insurance when you use your card to book your flights (or pay the taxes and fees on award flights ). And you may even be using one of these cards to book your trips. But you may not know what is and isn't covered by these benefits when your travel doesn't go smoothly.

In this guide, I'll give a high-level overview of some scenarios where you can — and can't — expect your credit card's travel insurance benefits to assist.

Sign up for our daily newsletter for more TPG news delivered each morning to your inbox.

Credit card travel insurance

We've written entire articles about credit cards that provide travel insurance . So, I recommend checking out the following stories to learn more about the travel insurance provided by top travel rewards cards :

- What your credit card's trip protection covers — and what it doesn't

- Flight delayed? Remember these 4 things if you want trip delay reimbursement from your credit card

- Flight delayed or canceled? Here are the best credit cards with trip delay reimbursement

- When to buy travel insurance versus when to rely on credit card protections

But, the protections provided by each card are different. So I recommend reading — or at least skimming — your card's guide to benefits before your next trip to familiarize yourself with those specifics. You can call the number on the back of your card for a physical copy or link if needed.

Cards like the Capital One Venture X Rewards Credit Card, Chase Sapphire Preferred Card, Ink Business Preferred Credit Card and The Platinum Card® from American Express provide excellent travel protections. But, I believe the Chase Sapphire Reserve provides the best travel insurance overall.

In this guide, I'll discuss how the benefits offered to Chase Sapphire Reserve cardholders (see the Chase Sapphire Reserve guide to benefits here) would help (or not) in several scenarios. If you generally pay for your travel with a different card, consider how the benefits on your card may differ.

Related: Travel is tricky right now — here are 7 mistakes to avoid on your next trip

4 times when your credit card's travel insurance can help

If your travel doesn't go smoothly this summer, benefits from your travel rewards credit card may offer reimbursement or other help. Here are four real-life scenarios where your credit card's travel insurance may come in handy.

Your flight is significantly delayed or canceled

First, the bad news: You'll need to work with your airline to get rebooked if your flight is canceled. And if your flight is significantly delayed, you'll need to either wait out the delay or work with your airline to get rebooked on a different flight.

But, the good news is that some cards offer trip delay reimbursement when you use your card to pay for your flight (or the taxes and fees on an award ticket). And this benefit can help as you wait for your delayed or rebooked flight.

For example, if you used the Chase Sapphire Reserve to book your original flight, Chase may reimburse you for "reasonable expenses incurred during the delay." In particular, you can get up to $500 per ticket when you're delayed for more than six hours or your delay forces you into an overnight stay. Chase says reasonable expenses include "meals, lodging, toiletries and medication."

But, you'll only be covered if you are delayed due to "equipment failure, inclement weather, strike [or] hijacking/skyjacking." So, if you're delayed due to the crew timing out during inclement weather, you'll be covered. But if the airline simply can't find any crew to operate your flight and doesn't provide you documentation stating the delay or cancellation is due to one of the aforementioned eligible reasons, you won't be covered.

Related: Chase paid for my $1,100-per-night hotel room thanks to built-in trip delay coverage

Your baggage is significantly delayed

Once again, let's discuss the bad news first: You must report your delayed baggage to the travel supplier. For example, if your checked baggage doesn't appear on the belt after your flight, you'll need to go to the airline's baggage office and fill out a report.

Usually, the airline will start trying to locate your baggage at this point. But often, the airline won't offer to reimburse you for any essentials you might need while you're separated from your baggage.

Luckily, some credit cards cover baggage delays . For example, if you used the Chase Sapphire Reserve to book your flight, Chase may reimburse you "for the emergency purchase of essential items, such as toiletries, clothing, and chargers for electronic devices (limit one per device)."

In particular, Chase may reimburse you up to $100 per day for up to five days. To qualify for this coverage, your baggage must be "delayed or misdirected" for at least six hours.

The items you purchase and include for reimbursement should be "essential." But, Chase excludes some items from reimbursement, including hearing aids, artificial teeth, prosthetic devices, tickets, jewelry, electronics and recreational equipment.

Related: What to do when your luggage is delayed or lost by an airline

You must cancel or interrupt a trip

First things first: No credit card offers " cancel for any reason " trip insurance as a complimentary benefit. But, if you must cancel or interrupt your trip for specific reasons, Chase Sapphire Reserve cardholders might be eligible for reimbursement of "nonrefundable prepaid travel expenses charged by a travel supplier" and "redeposit fees imposed by a rewards program administrator." And in the case of trip interruption, cardholders can be reimbursed change fees and costs to return a vehicle to their residence or the closest rental agency.

Many credit cards offer trip cancellation and interruption insurance . But, you'll only be eligible for reimbursement if you must cancel or interrupt your trip for specific reasons listed in the guide to benefits. For example, you may be eligible for reimbursement if you can't postpone or waive a call to jury duty or subpoena from the courts, and you prepaid for nonrefundable travel expenses with your Chase Sapphire Reserve.

Related: American Express adds new 'cancel for any reason' coverage option on flights

Your luggage is lost or damaged

Earlier, I discussed a scenario where your baggage is delayed. But, it's also possible that your luggage becomes lost, stolen or damaged. As with delayed baggage, you'll need to file a claim with the travel provider once you discover the issue.

Some travel providers will provide reimbursement to repair or replace your luggage. But, if the reimbursement isn't enough, you can also seek additional reimbursement via the baggage insurance offered by your credit card. If you booked your travel with your Chase Sapphire Reserve, you could get up to $3,000 per traveler per trip.

Related: The airline couldn't find my luggage — luckily I had Apple AirTags

7 times your credit card's travel insurance won't help

Of course, your credit card's travel insurance won't help you in every situation. Although you may still find relief through your travel provider or individual travel insurance , here are some real-world scenarios where you wouldn't be covered by the Chase Sapphire Reserve's travel protections :

- You want to be on a different flight: Flight delays and cancellations are frustrating. But, you'll need to work with your airline to get on a different flight. None of the trip delay insurance offered by credit cards will let you buy a new flight and then reimburse it.

- Staffing issues lead the airline to delay or cancel your flight: According to the Chase Sapphire Reserve's guide to benefits, only delays to your trip that are caused by "equipment failure, inclement weather, strike [or] hijacking/skyjacking" are eligible for trip delay reimbursement. So, if the airline can't find crew for your flight due to its employees being sick, for example, you won't be covered.

- Your lodging canceled on you: It's frustrating to be walked from a hotel or have your lodging canceled on you. After all, you may face much higher prices if you need to book a new stay. But, except in specific cases covered by trip cancellation and interruption insurance — such as if your lodging at your trip's destination is "made uninhabitable" — your credit card benefits aren't going to help.

- Your common carrier or travel insurance policy already provides what you need: As an example, if you are delayed overnight and the airline provides you with hotel and meal vouchers, you can't claim reimbursement for these same expenses through your credit card's trip delay benefit . The Chase Sapphire Reserve's guide to benefits states the trip delay benefit "applies to reasonable expenses incurred during your delay not otherwise covered by your common carrier, another party or your primary personal insurance policy."

- Your delay caused you to miss things you already paid for: Trip delays may cause you to miss shows, activities, separately booked flights, hotel nights and more. But, the Chase Sapphire Reserve's trip delay benefit is only for reasonable expenses you incur during your delay. As such, any prepaid trip expenses won't be covered.

- You have to cancel or interrupt your trip for a noncovered reason: As discussed above, the trip cancellation and interruption insurance offered by credit cards like the Chase Sapphire Reserve only covers you if you need to cancel or interrupt your trip for select reasons. So, if you need to cancel or interrupt your trip for other reasons, your credit card's travel insurance won't help. For example, you wouldn't be covered by the Chase Sapphire Reserve's insurance if you didn't obtain a necessary visa or your airline became financially insolvent.

- You left an item or bag behind on the train, airplane or boat: Although some Amex cards include recently purchased items you lose under purchase protection insurance , most travel insurance offered by credit cards won't reimburse you for items you inadvertently left behind.

Travel insurance benefits vary from card to card, though. And, only select family members may be covered along with you for some benefits. So take a look at your card's guide to benefits or call the number on the back of your credit card to learn whether your specific scenario will be covered.

Related: 8 times your credit card's travel insurance might not cover you

Bottom line

Of course, this article assumes you used a credit card with travel insurance to pay for your trip, and the exact protections vary from card to card. But hopefully, this guide gave you an idea of the types of help you may get from your credit card's travel insurance if things go wrong with a trip this summer or beyond.

Finally, some premium travel cards offer an additional perk that may help if you face troubles this summer: lounge access . It can be much more relaxing to wait out a delay in the comfort of a lounge. Plus, you may gain access to agents that can help you rebook or handle complicated bookings if you have access to your airline's lounge.

For Capital One products listed on this page, some of the above benefits are provided by Visa® or Mastercard® and may vary by product. See the respective Guide to Benefits for details, as terms and exclusions apply

This browser is not supported. Please use another browser to view this site.

- All Save & Spending

- Credit cards

- Newcomers to Canada

- All Investing

- ETF finder tool

- Best crypto

- Couch potato

- Fixed rates

- Variable rates

- Mortgage calculator

- Income property

- Renovations + maintenance

- All Insurance

- All Personal Finance

- Finance basics

- Compound interest calculator

- Household finances

- All Resources + Guides

- Find a Qualified Advisor

- Monthly budget template

- ETF Finder Tool

- Student money

- First-time home buyers

- Guide For New Immigrants

- Best dividend stocks

- Best online brokers

- Where to buy real estate

- Best robo-advisors

- All Columns

- Making sense of the markets

- Ask a Planner

- A Rich Life

- Interviews + profiles

- Retired Money

The best travel insurance credit cards in Canada for 2024

Searching for the perfect card? Compare your options with our interactive tool, and filter results based on rewards value, annual fees, income requirements, and more.

Travel medical emergency insurance for trips up to 60 days with insurance options also available for seniors (rare among travel cards).

Travel insurance for trips up to 25 days. Plus receive airport lounge and noforex perks.

Among the few no fee credit cards to offer comprehensive travel insurance (for trips of up to 10 days). Plus get a $50 cash bonus upon approval with Ratehub.ca.

MoneySense is an award-winning magazine, helping Canadians navigate money matters since 1999. Our editorial team of trained journalists works closely with leading personal finance experts in Canada. To help you find the best financial products, we compare the offerings from over 12 major institutions, including banks, credit unions and card issuers. Learn more about our advertising and trusted partners .

Advertisement

Best credit cards for travel insurance by category

By Keph Senett on May 17, 2024 Estimated reading time: 5 minutes

If you’re one of the nearly 80% of Canadians planning a trip outside your province or territory this year, you’re going to want to use a travel credit card with solid insurance. The types of coverage you’ll need—and the perks and benefits that are most valuable to you—will depend on the type of trip you’re taking, so we’ve broken down our favourites into categories.

Best travel insurance credit card overall

At a glance: The National Bank World Elite Mastercard doubles the insurance coverage you get with many other cards, including many on this list. Not only does it offer a wide range of insurance coverages—from emergency medical to trip cancelling, baggage delay and car rental coverage—but the coverage amounts are also impressive (case in point: $5,000 in trip cancellation coverage). Most notable is the duration of emergency medical coverage, including for seniors over the age of 65.

National Bank World Elite Mastercard

- Annual fee: $150

- Earn rate: 5 points per $1 on grocery and restaurant purchases; 2 points per $1 on gas, EV charges, recurring bill payments and travel booked through À La Carte Rewards; and 1 point per $1 on all other purchases.

- Welcome offer: You can earn up to 40,000 rewards points. Must apply by August 15, 2024.

- Annual income requirement: Personal income of $80,000 or household income of $150,000

- Recommended credit score: 760 or higher

- Interest rates: 20.99% on purchases, 22.49% on cash advances, 22.49% on balance transfers

- Travellers with the National Bank World Elite Mastercard get $5 million in emergency medical coverage for trips of up to 60 days, which is three times longer than many other top-tier travel insurance cards.

- With other cards, the coverage period for travellers aged 65 and older is typically very short, around 3 to 5 days. With this card, seniors are covered for trips of up to 15 days—more than three times as long—until they reach the age of 75.

- The car rental insurance coverage applies to rentals of up to 48 days, which is longer than most other cards.

- You’re covered against inconveniences during your travels, with above-average trip cancellation coverage of $2,500 and trip interruption coverage of $5,000.

- The card’s inventive travel fee reimbursements system can cover you for up to $150 annually for travel-related costs like airport parking, seat selection, and checked baggage fees.

- Cardholders have unlimited access to the National Bank Lounge at the Pierre Elliott Trudeau airport in Montreal.

- This card doesn’t come with travel accident coverage, which means you wouldn’t be covered for injuries that occur while travelling on a common carrier, such as an airplane or train.

- The annual fee of $150 is higher than some other cards in this category.

- The income requirements are high, at $80,000 personal or $150,000 for the household.

Honourable mentions: Best travel insurance cards with an annual fee

At a glance: It would be hard to overstate the perks of lounge access. When you use this card for your travel expenses, you get just that: a worry-free haven. The Scotiabank Passport Travel Visa Infinite is a top-notch travel card in its own right, offering a solid suite of travel and car rental insurance coverage. Those under 65 get up to 25 days of travel medical insurance, which is impressive compared to some other cards on this list. If you’re aged 65 or older though, you are only covered for three days. The card also boasts coverage for trip cancellation, flight delays, lost baggage, rental car collision/ damage, accident insurance and more.

Scotiabank Passport Visa Infinite

- Annual fee: $150

- Earn rate : 3 Scene+ points per $1 spent at Sobeys stores; 2 points per $1 on groceries, dining, entertainment and transit; 1 point per $1 on everything else. Plus, pay no FX fees

- Welcome offer: earn up to $1,300 in value in the first 12 months, including up to 40,000 bonus Scene+ points and first year annual fee waived. Offer ends July 1, 2024.

- Annual income requirement: Personal income of $60,000 or household income of $100,000

- Point value: 1 Scene+ point = $0.01 when redeemed for travel, store purchases and food and drink at Cineplex and Scene partners

- Recommended credit score for approval : 700 or higher

- Interest rates: 20.99% on purchases, 22.99% on cash advances, 22.99% on balance transfers

- Comes with complimentary Visa Airport Companion membership and six lounge passes per year, good for more than 1,200 lounges worldwide.

- You won’t be charged a foreign exchange fee on purchases made in other currencies.

- This card has a good insurance offering that includes up to 25 days of travel medical insurance for those under 65 years of age plus trip cancellation, flight delays, lost baggage, rental car collision/ damage, accident insurance and more.

- Travelers aged 65 or older are only eligible for three days of travel medical insurance.

- The rewards on offer here are lower than what’s offered with some other premium credit cards.

- The $60,000 personal or $100,000 household income requirements will be out of reach for some.

At a glance: Canadians are privileged when it comes to healthcare, so it’s no surprise we want to travel with robust medical insurance. While many credit cards offer medical coverage of up to $1 million, the Ascend World Elite Mastercard doubles that, offering $5 million in coverage for up to 21 days of travel—on unlimited trips per year. You’ll also get travel accident insurance, which covers you and your spouse and dependants for up to $500,000 on passenger planes, busses, taxis, trains and cruise ships.

BMO Ascend World Elite Mastercard

- Earn rates: 5 points per $1 spent on eligible travel purchases; 3 points per $1 on dining, entertainment, and recurring bill payments; 1 point per $1 on everything else

- Welcome bonus: You can earn up to 100,000 points

- Points values: 1 BMO Rewards point = $0.0067 when redeemed for travel

- Interest rates: 20.99% on purchases, 23.99% on cash advances, 23.99% on balance transfers

- The Ascend World Elite Mastercard offers $5 million in coverage for up to 21 days of travel—on unlimited trips per year.

- With the delayed and loss baggage insurance you’ll be reimbursed up to $500 per insured person if your bags are lost or damaged, and if your checked bags are delayed more than 6 hours, you’ll get $500 to purchase essentials, too.

- Includes membership in Mastercard Travel Pass and comes with four free passes annually.

- You can get a discount of up to seven cents per litre at Shell when you pay with this card.

- After your first four lounge passes, you’ll have to pay US$32 per visit.

- This card has an annual fee of $150, which is higher than some other cards in this category.

At a glance: Many travel credit cards focus on air travel but for the road trippers among us, we’ve selected the BMO CashBack World Elite Mastercard. Cardmembers are covered by the BMO World Elite Total Travel and Medical Protection package, which includes collision damage waiver benefits on rental cars and eight days of out-of-province and out-of-country emergency medical benefits up to $5 million. Plus, it includes a free, basic membership in the Dominion Automobile Association and the benefits of its BMO Roadside Assistance Program.

BMO CashBack World Elite Mastercard

- Annual fee: $120

- Earn rate: 5% cash back on groceries, 4% back on transit, 3% back on gas and electric vehicle charging, 2% on recurring bill payments, and 1% back on everything else

- Welcome bonus: You can earn up to 10% cash back in your first 3 months and the $120 annual fee waived in your first anniversary

- Additional benefits : Complimentary Roadside Assistance Program; BMO World Elite Total Travel and Medical Protection; 25% off at National and Alamo for car rentals; and Mastercard Travel Rewards program.

- Cardmembers are covered by the BMO World Elite Total Travel and Medical Protection package, which includes collision damage waiver benefits on rental cars and eight days of out-of-province and out-of-country emergency medical benefits up to $5 million.

- Includes a free, basic membership in the Dominion Automobile Association and the benefits of its BMO Roadside Assistance Program.

- At 5%, this card has the highest cash back earn rate on groceries in Canada.

- Lets you earn cash back in frequently used categories which you can redeem on demand.

- Although this card offers extremely competitive earn rates, there are low monthly caps on bonus categories: $500 in groceries, $300 in transit, gas, and EV charging, and $500 in recurring bills. Any purchases over these monthly limits will earn at the 1% base rate.

At a glance: The TD First Class Travel Visa Infinite offers up to $1,500 per person in trip cancellation insurance. This, along with the medical insurance coverage, common carrier travel accident protection, delayed or lost baggage coverage, and travel assistance, should help you rest easy as you plan your travel.

TD First Class Travel Visa Infinite Card

- Annual fee: $139 (annual fee rebate—conditions apply to qualify)

- Earn rates: Up to 8 TD Rewards points per $1 on travel; 6 points per $1 on groceries and restaurants; 4 points per $1 on recurring bills; and 2 points per $1 on all other purchases

- Welcome offer: You can earn up to $700 in value, including up to 75,000 TD Rewards Points and no Annual Fee for the first year. Conditions Apply. Account must be approved by September 3, 2024. Plus, you get an annual birthday bonus of 10% of your previous year’s points (up to 10,000 points).

- Point value: 1 TD Rewards point = $0.005 when redeemed for travel via Expedia For TD or $0.004 when redeemed through other providers and websites

- Recommended credit score for approval: 725 or higher

Best no-fee travel insurance credit card

At a glance: If you want a travel insurance credit card without committing to an annual fee, check out the Rogers Red World Elite Mastercard. Not only does this no-fee card include valuable travel and rental car insurance with perks like free Boingo Wi-Fi, it’s also a cash back card. This means that for every $1 you spend on the card you’ll get back 1.5% (or 2% if you’re a Rogers, Fido or Shaw customer).

Rogers Red World Elite Mastercard

- Annual fee: $0

- Earn rate: 1.5% cash back on all purchases, or 2% back for Rogers, Fido and Shaw customers; 3% cash back on all purchases in U SD

- Welcome bonus: This card does not have a welcome bonus at this time.

- Annual income requirement: Personal income of $80,000 or household income of $150,000

- Cards with no annual fee usually don’t come with travel insurance, but this card comes with six types of coverage, including emergency medical for up to 10 days, and car rental theft and damage coverage for up to 31 days.

- You can earn 1.5% cash back on all your purchases (or 2% if you’re a Rogers, Fido or Shaw customer). Plus, with 3% cash back on transactions in U.S. dollars, you’ll save on foreign transaction fees, too.

- Whereas most World Elite cards come with an annual fee, the Rogers Red gives you World Elite benefits like discounts on Booking.com and free Boingo Wi-Fi at no cost.

To be approved, you’ll need a personal income of at least $80,000 or household income of at least $150,000.

How does credit card travel insurance work?

Every insurance package is tailored to a specific card and program but in general, the process is simple. You’ll usually have to book your travel on that credit card but different cards have different rules. For example, some say you need to book 100% of your trip on the card while others don’t have that stipulation. Read your documents to determine your responsibilities. Once you book, you’ll automatically have access to the included coverage. You don’t have to notify the credit card company that you’re traveling or call to activate the coverage. That said, we always recommend that you read the documentation from your credit card company.

More of Canada’s best credit cards :

- Canada’s best credit cards

- Canada’s best credit cards for gas

- Canada’s best credit cards for grocery purchases

- Canada’s best cash back credit cards

What does the * mean?

Affiliate (monetized) links can sometimes result in a payment to MoneySense (owned by Ratehub Inc.), which helps our website stay free to our users. If a link has an asterisk (*) or is labelled as “Featured,” it is an affiliate link. If a link is labelled as “Sponsored,” it is a paid placement, which may or may not have an affiliate link. Our editorial content will never be influenced by these links. We are committed to looking at all available products in the market. Where a product ranks in our article, and whether or not it’s included in the first place, is never driven by compensation. For more details, read our MoneySense Monetization policy.

About Keph Senett

- Our Bloggers

Select Page

TD Travel Medical Insurance with your TD Credit Card

Posted by Maple Miles | Nov 3, 2023 | Travel Tips | 0

I have summarized a few important details as you evaluate whether you need additional emergency medical insurance during your travels.

The following credit cards have the Travel Medical Insurance coverage with TD:

- TD Aeroplan Visa Infinite ( Certificate of Insurance )

- TD First Class Travel Visa Infinite ( Certificate of Insurance )

- TD Cash Back Visa Infinite ( Certificate of Insurance )

- TD Aeroplan Visa Infinite Privilege ( Certificate of Insurance )

The information listed below is my interpretation of the insurance policy.

For other credit card issuers, information about their travel insurance policy is available here:

- American Express Out of Province and Country Emergency Medical Insurance

- BMO Out of Province Emergency Medical Protection Insurance

- CIBC Out of Province Emergency Medical Travel Insurance

- RBC Out of Province Emergency Medical Travel Insurance

- Scotiabank Travel Emergency Medical Insurance

- TD Travel Medical Insurance

Coverage Eligibility

The basic coverage provided for all the listed cards are:

- Coverage is provided to the cardholder, cardholder’s spouse, and cardholder’s dependent children.

- Coverage is limited to $2,000,000.

- The dependent children do not need to be traveling with the cardholder or the cardholder’s spouse.

- Additional cardholders are covered as well.

Exclusions of Basic Coverage

Important Exclusions:

- Pre-existing medical conditions need to be stable at least 90 days prior to your trip departure date, for those under 65, or 180 days, for those 65 or older.

- Scuba diving (unless you have a designation), motorized race, motorized speed contest, bungee jumping, parachuting, rock climbing, mountain climbing, hang-gliding or skydiving, amongst other sports and high risk activities.

Coverage Benefits

Differences between cards.

The major difference between the credit cards is what is the age group that is covered by the insurance and how long they are covered for.

One unique situation about the TD credit cards are that the benefits are extended to the dependent children and spouse, and even additional cardholders, even if they are not traveling with the cardholder.

Join our mailing list to receive the latest news and updates from our team.

You have successfully subscribed, maple miles.

Hello Hello, this is Moli! Welcome to Maple Miles. A tech professional on a weekday, and a global traveler outside of work. I manage my entire family's travel, connecting us across the globe, between Canada (Vancouver is home, for now), India and whatever country comes in between. I love water, so you might always find me either dreaming of a beach, or actually at a beach in my free time.

More Posts from Maple Miles

Oh, Hello from Maple Miles

March 8, 2023

Best Ways to Earn Free WestJet Flights

March 9, 2023

WestJet Companion Voucher: How to earn them?

This site uses Akismet to reduce spam. Learn how your comment data is processed .

Most Popular Posts

Our Authors

The Unaccompanied Flyer

Travel Gadget Reviews

The Flight Detective

Takeoff To Travel

The Hotelion

Bucket List Traveler

MJ on Travel

The Points Pundit

Family Flys Free

Recent Reviews

- St Regis Cairo Review – A perfect stay Score: 100%

- Six Passengers in Two Business Class Seats in Gulf Air Score: 90%

- Review: Hyatt Place Waikiki Score: 83%

- Review: Hyatt Centric Waikiki Score: 81%

- Gulf Air Business Class from Mumbai to Bahrain Score: 65%

- Book Travel

- Credit Cards

Which Credit Cards Have the Best Insurance for Seniors?

Insurance coverage offered by credit cards often doesn’t get the same attention as a card’s other benefits. However, it’s an important element to be aware of, particularly for travellers over the age of 65.

While some insurance coverage is fairly comparable among credit cards within the same tier, this isn’t the case when it comes to emergency medical coverage, which can differ dramatically between the cards.

In this guide, we’ll outline the best options for securing coverage for you or your loved ones.

Emergency Medical Care Outside of Your Province of Residence

Before delving into the cards themselves, it’s important to go over what this insurance covers, and to establish a baseline of the lower-end of what you can expect in terms of coverage.

Emergency medical care insurance coverage is designed to reimburse you for a certain dollar amount in the event that you’re injured or experience a medical emergency while travelling outside your home province.

This coverage becomes even more relevant if you’re travelling internationally, where it may be more difficult to navigate and understand the local medical system and its costs.

With coverage, not only do you have peace of mind when you travel, but you can also prioritize getting care without worry, should you run into some bad luck.

As we mentioned above, the emergency medical care coverage can vary considerably across different credit cards; therefore, to establish a baseline from which to compare, let’s first look at the coverage offered by two popular cards.

Our first example, the American Express Cobalt Card, offers emergency medical coverage for the first 15 consecutive days of your trip if you’re 64 years old or under; however, once the cardholder turns 65, there’s no coverage at all.

Looking at higher-end cards, the TD Aeroplan® Visa Infinite Privilege* Card offers emergency medical coverage for an incrementally better four days if you’re 65 or older.

As we can see, neither of these cards offers much in the way of emergency medical coverage for travellers over 65.

Therefore, you’ll want to consider a credit card that provides the best insurance for anyone travelling in their golden years.

As always, be sure to read the card’s insurance booklet to understand what’s covered in your specific situation. If you ever have any questions, reach out to the card issuer to confirm what’s included.

National Bank World Elite Mastercard

In Canada, the gold standard of insurance coverage is set by the National Bank World Elite Mastercard. Travellers over 65 years old are covered for up to 15 days when travelling out of province. The coverage lasts until you turn 76, at which point you’re no longer covered.

It’s also important to note that if you have a pre-existing illness or injury or if there have been changes to your health within six months of your departure date, you won’t be covered if you suffer an accident directly or indirectly related to the pre-existing condition.

If you qualify for coverage, National Bank will cover you up to $5,000,000 for emergency medical care if you end up needing it.

We consider the National Bank World Elite Mastercard as the best credit card for insurance in Canada. If you make a booking with points, you’ll also be covered, which is another one of the card’s mainstay features.

- Earn 5,000 À la carte Rewards points upon signing up for insurance payments for at least the first three months†

- And, earn 10,000 À la carte Rewards points upon spending $10,000 in the first six months†

- And, earn 20,000 À la carte Rewards points upon spending $20,000 in the first 12 months†

- Earn 5 x À la carte Rewards points on grocery and restaurant spend†

- Get travel insurance on award travel, as well as medical coverage on longer trips for ages up to 75†

- Receive $150 in annual credits for airport parking, baggage fees, seat selection fees, lounge access, and airline ticket upgrades†

- Minimum income: $80,000 personal or $150,000 household

- Annual fee: $150

HSBC World Elite Mastercard

The HSBC World Elite Mastercard has historically been another staple in Canadians’ wallets, due to its lack of foreign exchange fees. However, following the announcement that RBC would acquire HSBC, the card has subsequently been closed to new applications as of October 2023.

It’s unclear what the future holds for this and other HSBC cards, but if you’re currently a cardholder, then it’s business as usual until we hear otherwise.

This is good news, as the HSBC World Elite Mastercard also has quite a generous policy when it comes to emergency medical coverage for seniors.

For people 65 years of age or older, you receive emergency medical coverage for up to 21 consecutive days after you leave your province of residence. This is an improvement over the length of coverage from the National Bank World Elite Mastercard, and there’s no upper limit specified for age, which is outstanding.

While HSBC has a more favourable inclusion list, the insurance coverage is less, at $2,000,000 instead of the $5,000,000 offered by National Bank.

Combined with no foreign transaction fees, competitive earning rates, and generous insurance policy for seniors, it’s no wonder the HSBC World Elite Mastercard was such a popular choice among Canadians.

Desjardins Odyssey Visa Infinite Privilege

A less talked about card that deserves a spot on this list is the Desjardins Odyssey Visa Infinite Privilege Card, which has a similar insurance structure to the National Bank World Elite Mastercard.

If you’re 65 or older, you’re eligible for emergency medical coverage for up to 15 days from when you leave the province in which you reside. However, once you turn 76, you would no longer be eligible for any coverage.

You’ll be covered up to a maximum of $5,000,000 per person, excluding situations where you have a pre-existing condition, in which case, you won’t be covered if your accident while travelling is related to said condition.

Note that your pre-existing condition window goes back 182 days from date of departure.

Unlike the other cards on this list, the Desjardins Odyssey Visa Infinite Privilege is a cash back card, rather than a travel-focused card. It has an annual fee of $295 (CAD) for members, or $395 (CAD) for non-members, which is a fairly steep fee to pay.

- Earn 4% cash back on restaurant purchases

- Earn 3% cash back on grocery and travel purchases

- Earn 1.75% cash back on everything else

- Access DragonPass airport lounges with six complimentary visits

- Best in-class medical and travel insurance coverage

- Minimum income: $200,000 household

- Annual fee: $395

CIBC Aeroplan® Visa Infinite Privilege* Card

When it comes to emergency medical coverage, especially for those older than 65, the CIBC Aeroplan® Visa Infinite Privilege* Card comes out ahead of its premium Aeroplan co-branded credit card counterparts.

The CIBC Aeroplan® Visa Infinite Privilege* Card offers 10 consecutive days of coverage for people 65 or older, which is more than its TD counterpart’s four days of coverage.

As usual, pre-existing conditions exclude you from coverage if your emergency is related or indirectly related to your existing condition.

However, keep in mind that unlike the National Bank World Elite Mastercard or the Desjardins Odyssey Visa Infinite Privilege Card, there’s no specified age maximum for coverage. Therefore, you’ll still be eligible for insurance, even if you’re over the age of 76.

This card is a great addition to your wallet if you tend to make shorter trips away from home, and want to remain in the Aeroplan ecosystem.

You’ll also enjoy benefits like lounge access, priority services, and a free checked bag when travelling with Air Canada.

- Earn 20,000 Aeroplan points upon first purchase †

- Earn 30,000 Aeroplan points upon spending $15,000 in the first four months †

- Plus, earn an anniversary bonus of 30,000 Aeroplan points upon renewing the card for a second year, after having spent at least $25,000 in the first year †

- Earn 2x Aeroplan points on Air Canada purchases †

- Earn 1.5x Aeroplan points on gas, groceries, dining, food delivery, electric vehicle charging, and other travel purchases †

- Aeroplan preferred pricing, free checked bag, priority check-in and boarding on Air Canada flights †

- Unlimited Air Canada Maple Leaf Lounge access †

- DragonPass membership with six free lounge visits per year †

- NEXUS application credit †

- Minimum income: $150,000 personal or $200,000 household

- Annual fee: $599

While most credit cards don’t offer travel insurance coverage for travellers over the age of 65, and even fewer cover those who are 76 and older, there are still a few standout cards that extend emergency medical protection to travellers in their golden years.

Having emergency medical coverage while you’re travelling is an important way to stay safe and healthy, and to provide yourself and your loved ones with peace of mind.

No matter your age, there’s a card out there that will extend some sort of coverage to you, so make sure to keep that in mind before embarking on your next adventure.

- Earn 80,000 MR points upon spending $15,000 in the first three months

- Plus, earn 40,000 MR points upon making a purchase in months 14–17 as a cardholder

- And, earn 1.25x MR points on all purchases

- Also, receive a $200 annual travel credit

- Transfer MR points to Aeroplan and other frequent flyer programs for premium flights

- Unlimited airport lounge access for you and one guest at Priority Pass, Plaza Premium, Centurion, and other lounges

- Credits and rebates for business expenses throughout the year with Amex Offers

- Bonus MR points for referring family and friends

- Qualify for the card as a sole proprietor

- Annual fee: $799

Go through the insurance with a highlight marker, and then mark your concerns. Get answers to your questions before you go. For pre-existing conditions, some only allow them to be stable for 3 months beforehand, others 6 months.

Thanks for the article

Speaking as a senior, I would never rely on a credit card for emergency medical travel insurance. Most seniors are on some sort of medication and/or have pre-existing conditions. Most travel insurance, both CC and private, has a long list of conditions and exclusions. You usually only find out about them AFTER you make a claim.

If you’re concerned about emergency medical situations when you travel outside Canada, then find a travel insurer who will cover you without excluding pre-existing conditions or at least make sure they tell you beforehand what you’re actually covered for based on your specific medical conditions. Naturally, expect to pay more, perhaps a lot more, than younger people for coverage that you can actually rely on should you need it.

Otherwise you’re just gambling.

Your email address will not be published. Required fields are marked *

Save my name, email, and website in this browser for the next time I comment.

Prince of Travel is Canada’s leading resource for using frequent flyer miles, credit card points, and loyalty programs to travel the world at a fraction of the price.

Join our Sunday newsletter below to get weekly updates delivered straight to your inbox.

Have a question? Just ask.

Business Platinum Card from American Express

120,000 MR points

American Express Aeroplan Reserve Card

85,000 Aeroplan points

American Express Platinum Card

100,000 MR points

TD® Aeroplan® Visa Infinite Privilege* Card

Up to 75,000 Aeroplan points†

Latest News

Aeroplan Extends No-Expiry Policy Through November 2025

News Jun 24, 2024

Singapore Airlines KrisFlyer: Spontaneous Escapes for July 2024

Deals Jun 24, 2024

Scotiabank Credit Card Offers: Earn Up to 40,000 Scene+ Points (Ending Soon)

Recent discussion, is flying in canada getting more expensive, getting us credit cards for canadians, air canada pauses changes to seat selection policy at check-in, anna rozenberg, the best ways to book aer lingus with avios, far-flung destinations you can reach with aeroplan points, prince of travel elites.

Points Consulting

Do I need credit card travel insurance?

Key takeaways.

- S ome typical travel insurance benefits include trip cancellation and interruption insurance, trip delay reimbursement, emergency medical coverage, emergency medical evacuation, lost or damaged baggage insurance, delayed baggage insurance and car rental insurance

- Many top travel credit cards provide enough travel insurance benefits to protect you in an emergency or if your plans change, so purchasing extra travel coverage likely won’t be necessary

- However, if you plan to book an expensive trip or travel abroad for an extended period of time, you might want to purchase travel coverage. Check with your card issuer to confirm any coverage terms and conditions before purchasing any additional policies

Now that travel is back in full swing, it’s time to plan your next exciting getaway. With all the fun that comes with traveling to new locales, you always risk running into expensive problems far from home. Lost luggage, canceled flights, injuries, rental car mishaps — all sorts of inconveniences can occur when traveling. One way to soften the blow of travel disasters — at least financially — is to have travel insurance.

What is travel insurance?

Travel insurance helps provide financial compensation for mishaps like lost or stolen luggage or if you need to cancel a trip for reasons that are beyond your control. In the event of a qualifying incident, you can file a claim with the insurance company to get money back for certain expenses, up to a previously agreed-upon limit. You can purchase travel insurance policies from insurance providers — or you can take advantage of travel insurance benefits offered by your credit card provider.

Fortunately for travelers, many credit cards offer some form of travel insurance to cardholders, and some of the top travel credit cards offer an impressive lineup of travel protections. However, credit card travel insurance works a bit differently than a travel insurance policy you purchase .

As a rule, credit card travel insurance doesn’t typically offer the same level of comprehensive coverage you’d get from a purchased policy. You also can’t choose what type of coverage you receive. That said, many travel credit cards offer some level of coverage for issues like trip cancellation and interruption , trip delays, lost luggage, baggage delays , rental cars and travel accidents.

If you’re considering buying separate travel insurance, it’s worth learning what type of coverage your credit card offers before paying for protection you may already have. One easy way to find out what your credit card covers is to call your credit card provider and have them walk you through your card’s benefits guide.

What is credit card travel insurance?

Credit card travel insurance is a complimentary benefit that commonly comes with credit cards. While it isn’t the most robust coverage, this protection can help out with various travel-related emergencies and inconveniences. When cardholders use their credit cards to book travel arrangements such as flights, hotels or rental cars, they may automatically become eligible for these insurance benefits. The key element here is to book at least your flights or other transportation using the credit card, or you won’t qualify for the coverage.

Typically, credit card travel insurance includes coverage for trip cancellations, trip interruptions and delays, as well as lost or delayed baggage. Some cards may also provide coverage for emergency medical expenses, evacuation and rental car insurance. The extent of coverage varies among credit cards and may depend on factors such as the card type, the issuer and the terms and conditions outlined in the card agreement.

It’s important for cardholders to review the specific details of the travel insurance offered by their credit cards, including any limitations, exclusions and requirements for activation. While credit card travel insurance can be a valuable perk, you may want to consider purchasing additional coverage for more thorough coverage.

What does travel insurance cover?

To make it easier to understand what travel insurance covers, we’re breaking down the most common types of coverage.

Coverage for canceled, interrupted or delayed trips

If you need to cancel your trip, having trip cancellation and interruption coverage can provide reimbursement for the cost of your trip, including expenses like transportation, hotels and prepaid activities. Qualifying reasons might include events such as the death of a family member, terrorism, natural disasters and unforeseen illnesses or injuries. Check your policy to see what’s included as each policy differs. In some cases, events like jury duty or being laid off from your job qualify.

Generally, your trip needs to be delayed unexpectedly by six to 12 hours (but this varies by each policy) to qualify for trip delay reimbursement. This benefit typically offers $150 to $200 per day for a certain number of days — though sometimes, this benefit offers a certain amount per ticket — to cover necessary expenses like lodgings or food.

Getting stranded far from home and having to pay for extra nights in a hotel you didn’t budget for, having to change flights at the last minute or canceling some or all of a nonrefundable trip before you even hit the road can all cost a pretty penny. If you’re traveling somewhere prone to major weather incidents and have multiple flights (increasing the possibility of missed connections), this is an important type of insurance to have.

Coverage for emergency medical situations

Emergency medical benefits can come in handy if you’re injured or become ill while traveling and require hospitalization, medication or treatment. This type of coverage is more necessary if you’re traveling internationally or on a cruise where you may not have access to medical care covered by your health insurance plan. Unfortunately, in most cases, you’ll need to pay for your medical care out of pocket and file a claim later for reimbursement.

If you have a medical emergency while traveling that requires transportation to the nearest medical facility, medical evacuation coverage can help with those costs. This is often add-on coverage for travel medical insurance, but it can come in handy if your treating physician recommends you go home to receive medical treatment or if a death occurs and there are costs associated with transporting the traveler’s remains.

Are you traveling out of network? How about out of the country or to a remote locale where it’s difficult to access medical care? If you need medical attention when you’re traveling and your health insurance won’t cover your costs, having travel insurance that pays for medical emergencies and medical transportation can save you a lot of money.

Coverage for lost, damaged or delayed baggage

Generally, lost or damaged baggage protection only covers up to a certain value, but your belongings are covered throughout your entire trip. Some policies only reimburse for luggage that is lost or damaged when it is checked with a common carrier. If your bag is permanently lost, having the right type of insurance can save you a lot of money. If you’ll be carrying more expensive items, you may want to pursue a third-party plan that will reimburse more expensive items, such as a camera or computer. Additionally, note that you may need to file a police report within a certain timeframe to receive coverage.

Even if your belongings eventually arrive in one piece, baggage delay protection can reimburse you for any costs you incur while waiting to be reunited with your belongings. You may face a daily limit on how much you can purchase to replace your delayed goods, along with a limit on what you can purchase. Additionally, these benefits don’t typically kick in unless your luggage is delayed for a specified period of time (usually six to 24 hours).

If you’re checking a bag while flying, you may want coverage for lost, damaged or delayed baggage. This coverage can help you pay for clothing, toiletries and any other items you need to replace if your luggage goes missing or is harmed, especially if it gets lost by the time you arrive at your destination. If you’re driving, however, you probably won’t need this type of coverage.

Coverage for rental cars

Many credit cards offer rental car coverage for collisions, loss and damage. It’s usually secondary coverage, meaning it kicks in after your primary auto insurance, and it usually excludes liability for damage to other property or for injuries to others. However, some credit cards offer primary coverage, which typically provides reimbursement up to a certain amount for theft and collision damage. Note that you’ll typically need to decline the car rental company’s insurance in order to receive coverage through your credit card.

For domestic travel, your existing auto insurance policy may cover any issues with rental cars, and it’ll likely kick in before an additional collision policy anyway. Check out what your insurer covers first before getting an additional policy. It’s also worth noting that your credit card rental car insurance may apply overseas. However, it would be wise to look into additional car rental protections, whether with a third-party insurer or at the rental counter, since some countries are excluded from credit card rental car coverage.

How to use credit card travel insurance

If a trip is partially or fully booked on your credit card — be sure to confirm booking standards with your card provider first — you may be able to access travel insurance benefits that come with your credit card . Here’s how to use your credit card travel insurance:

- Confirm your coverage. Before you file a claim, it’s helpful to brush up on your coverage. Your card should come with a benefits guide that outlines what type of travel coverage you have, including the maximum amount they’ll cover, exceptions to your coverage and how long you have to submit a claim (typically less than 60 days).

- Show receipts and necessary documentation. You’ll likely need to provide receipts when you file your claim if you want to get your money back. You might also need to provide key documentation such as showing how a loss occurred, correspondence with travel providers proving they won’t reimburse you, doctors’ notes, police reports or any other applicable paperwork.

- File the claim. Report any losses or situations to the benefits administrator within your policy’s claim time frame. Generally, you’ll download a claim form from the credit card provider’s website and submit evidence of the losses or situations for which you’re seeking reimbursement.

- Wait for a decision. Your credit card provider will contact you with a decision regarding your claim and, if approved, explain how it plans to distribute your funds.

When is travel insurance worth it?

Traveling is expensive, so it’s understandable if you’re wondering — is trip insurance worth it? Where or not you should purchase travel insurance in addition to the benefits your credit card offers depends on how much coverage you already have and what your risk tolerance is. Some premium credit cards offer robust travel coverage — such as emergency evacuation coverage, lost baggage coverage or trip cancellation and interruption insurance — whereas no-annual-fee credit cards typically offer basic coverage like roadside assistance.

Note that travel insurance policies tend to get more expensive as you age. So the flat annual fees you’ll pay for premium travel credit cards such as The Platinum Card® from American Express ($695 annual fee) and the Chase Sapphire Reserve® ($550 annual fee) make their travel coverage more valuable the older you get.

Consider what type of travel insurance you may need and what events and belongings you need to have insured. If you want basic coverage for smaller issues, such as covering costs incurred if your flight is delayed, then your credit card policy may do the trick. But if you have ambitious travel plans that involve bigger risks — like booking a nonrefundable international trip — then you’ll likely want to purchase a travel insurance policy that will allow you to cancel a trip for any reason.

When is travel insurance not worth it?

Depending on where you’re traveling and the type of trip you’re taking, travel insurance might not be necessary. For example, if your trip is completely refundable, trip interruption and cancellation insurance is likely not necessary. You may also not need any type of travel insurance if you’re taking a cheap or short domestic trip.

Additionally, if you’re traveling within the U.S., you likely won’t need additional medical coverage beyond your existing health insurance plan (though it would be good to check your policy first). If you’re traveling outside of the U.S., however, additional medical coverage — whether purchased or provided through a credit card — can be helpful in an emergency situation.

Should you get a top credit card for travel insurance?

Many travel credit cards can provide you with enough travel insurance benefits to protect you in an emergency or if your plans change, so purchasing extra travel coverage likely won’t be necessary. Of course, this depends on the type of trip you’re taking, among other factors.

If you’re looking for a new credit card and want one that provides solid travel insurance coverage, here are some of the best cards for travel insurance to consider:

Although travel insurance can be a great cardholder perk, it probably won’t be the main factor you’re considering when picking out a new credit card . While it’s nice for frequent travelers, you’ll want to look for a credit card that offers benefits you’ll use, such as a great rewards program, a sign-up bonus or intro APR offers. A card that rewards you for your regular spending may be more valuable in the long run than one that comes with a limited amount of travel insurance to cover the occasional trip.

While you can’t predict the exact cost of every future trip you plan, you probably have an idea of what kind of trips you take and what type of coverage they require. For example, if you love taking road trips in your trusty SUV and rarely rent a car or book a flight for a vacation, then you’re less likely to need car rental or baggage delay coverage. But having roadside assistance as a perk may give you much-needed peace of mind when you hit the open road. Look for a credit card that offers coverage in line with the way you travel most often.

There is no worse feeling than thinking you have insurance coverage, only to find you’re going to need to pay more out of pocket than you realized when something does go wrong. Double-check the fine print for the travel insurance coverage before relying on a credit card’s insurance perks. You’ll likely come across some potential exclusions.

Frequently asked questions (FAQs)

Travel insurance costs vary depending on the type of plan you select: Basic, middle tier or comprehensive. They also typically depend on factors like your trip’s total cost, how long you’re traveling for, where you’re traveling, how many people require coverage and travelers’ ages. In general, you can expect to pay anywhere from 4 percent to 11 percent of the total cost of your trip.